Market Recap: March 2026

April 02, 2026

Market commentary

- U.S. growth is decelerating but remains intact. Fourth quarter GDP has been revised further downward, partly reflecting disruption from the government shutdown.

- Hiring has cooled, yet layoffs remain limited, and consumer spending continues to hold up, supported by wealth effects and tax refunds.

- Inflation pressures are resurfacing, driven mainly by supply-side factors such as energy, food, and transportation rather than excess demand, with services inflation remaining more persistent than goods.

- Financial conditions are tightening gradually, reflecting private credit liquidity concerns, equity downside risk, and waning wealth effects.

- Escalation of the conflict in Iran poses a key near-term macro risk, primarily through its effects on energy markets, supply chains, and inflationary pressures.

Select economic and market data

Statistic (monthly unless noted) |

Current |

Previous |

|---|---|---|

| U.S. GDP (quarterly) | 0.7% | 4.4% |

| Consumer Confidence | 91.8 | 91.0 |

| Consumer Price Index Y/Y | 2.4% | 2.4% |

| Core PCE (x food & energy) | 3.1% | 3.0% |

| ISM Manufacturing Index | 52.7 | 52.4 |

| Unemployment Rate | 4.4% | 4.3% |

| 2-Year Treasury Yield | 3.80% | 3.38% |

| 10-Year Treasury Yield | 4.32% | 3.94% |

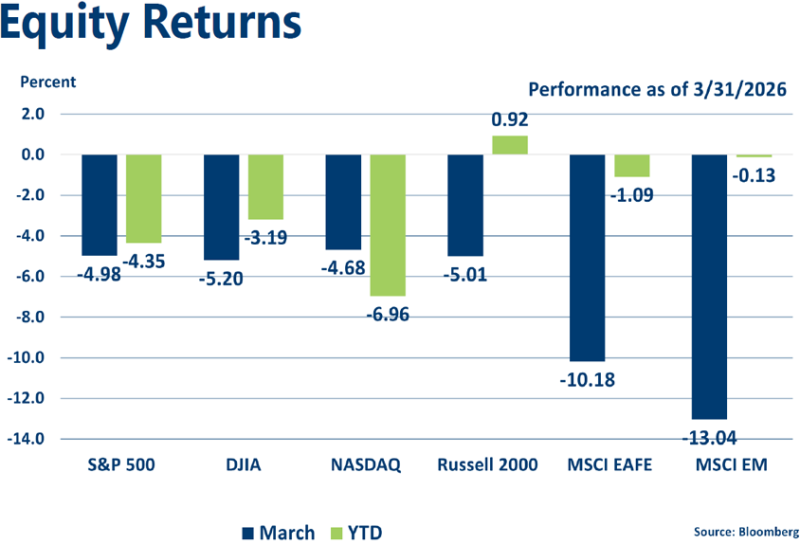

Equities

- U.S. stocks fell about 5% in March, with foreign markets underperforming due to their geographic exposure to the war and greater reliance on imported energy.

- Rising oil prices propelled the Energy sector (+10.3%) to the top spot in March, while all other S&P 500 sectors declined by at least 3.2%.

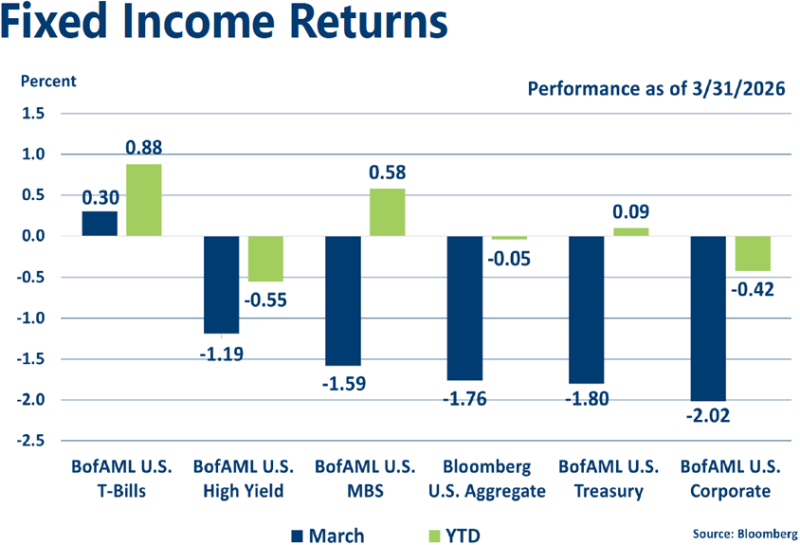

Fixed income

- The Fed remains on hold, with policymakers reluctant to tighten further amid slowing growth and unable to ease meaningfully while inflation remains elevated.

- Rising inflation concerns pushed bond yields sharply higher, resulting in mostly negative bond returns in March.

Strategic outlook

- Near-term caution toward equities is advisable, given heightened risks from geopolitical instability, trade uncertainty, and the potential for renewed inflationary pressures alongside an economic slowdown.

- Near-average expected returns projected for fixed income with the Fed on pause and rates reflective of economic conditions.

- Above-average volatility is likely given central bank involvement and geopolitical uncertainty.

|

Learning Center articles, guides, blogs, podcasts, and videos are for informational purposes only and are not an advertisement for a product or service. The accuracy and completeness is not guaranteed and does not constitute legal or tax advice. Please consult with your own tax, legal, and financial advisors.