Market Recap: June 2026

July 06, 2026

Market commentary

- The U.S. dollar index gained over 2% in June as the surprisingly hawkish tone from the new Fed Chair and higher U.S. yields pulled global capital back toward U.S. assets.

- May payrolls rose 172,000 jobs (three-month average now 188,000, the best in three years) with the unemployment rate holding at 4.3%, prompting a modest upgrade to the labor forecast.

- Conference Board Consumer Confidence ticked up to 91.2 from 90.6, and the University of Michigan sentiment index posted its first gain in four months as gasoline prices eased off recent highs.

- Labor market conditions remain stable, with low jobless claims and moderate hiring helping sustain economic resilience.

- Quarterly U.S. GDP jumped to 2.1% on stronger hours worked and business activity.

Select economic and market data

Statistic (monthly unless noted) |

Current |

Previous |

|---|---|---|

| U.S. GDP (quarterly) | 2.1% | 0.5% |

| Consumer Confidence | 91.2 | 90.6 |

| Consumer Price Index Y/Y | 4.2% | 3.8% |

| Core PCE (x food & energy) | 3.4% | 3.3% |

| ISM Manufacturing Index | 53.3 | 54.0 |

| Unemployment Rate | 4.3% | 4.3% |

| 2-Year Treasury Yield | 4.18% | 4.01% |

| 10-Year Treasury Yield | 4.47% | 4.44% |

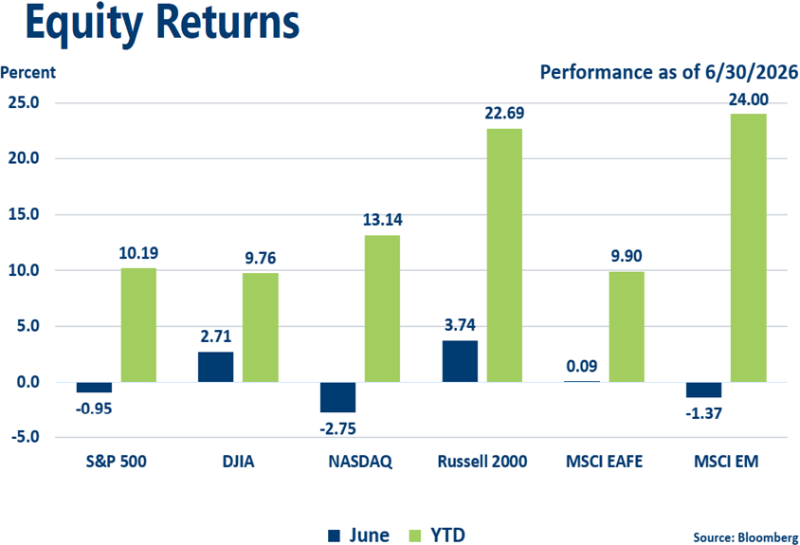

Equities

- U.S. equities pulled back modestly in June as a hawkish Fed surprise weighed on mega-cap tech, but the tape broadened meaningfully with small caps and the equal-weight S&P 500 outperforming, leaving the market up approximately 10% YTD heading into the second half of the year.

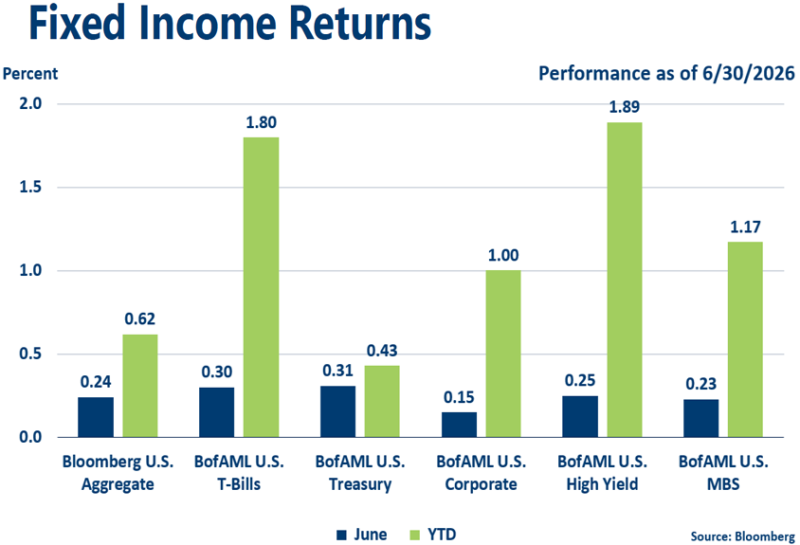

Fixed income

- U.S. Treasury yields drifted higher and the curve flattened in June, while corporate credit held remarkably firm with investment grade spreads near historic tights, high yield delivering positive returns, and default rates staying contained.

Strategic outlook

- Near-term caution toward equities is advisable, given heightened risks from geopolitical instability, trade uncertainty, and the potential for renewed inflationary pressures alongside an economic slowdown.

- Near-average expected returns projected for fixed income with the Fed on pause and rates reflective of economic conditions.

- Above-average volatility is likely given central bank involvement and geopolitical uncertainty.

|

Learning Center articles, guides, blogs, podcasts, and videos are for informational purposes only and are not an advertisement for a product or service. The accuracy and completeness is not guaranteed and does not constitute legal or tax advice. Please consult with your own tax, legal, and financial advisors.