Market Recap: May 2026

June 02, 2026

Market commentary

- The U.S. economy remains resilient, pointing to a mid-cycle slowdown — not a recession — supported by strong profits, low jobless claims, and steady growth.

- Consumer spending continues to outpace income, pushing the savings rate down to 2.6%, an unsustainable trend that suggests slower consumption ahead.

- Business investment — especially in AI and capital expenditures — remains strong, helping support overall economic activity.

- Labor market conditions remain stable, with low jobless claims and moderate hiring helping sustain economic resilience.

- Housing activity has softened amid declining sales, affordability pressures from higher mortgage rates, and rising inventory, though prices have begun to stabilize.

Select economic and market data

Statistic (monthly unless noted) |

Current |

Previous |

|---|---|---|

| U.S. GDP (quarterly) | 1.6% | 0.5% |

| Consumer Confidence | 93.1 | 93.8 |

| Consumer Price Index Y/Y | 3.8% | 3.3% |

| Core PCE (x food & energy) | 3.3% | 3.2% |

| ISM Manufacturing Index | 54.0 | 52.7 |

| Unemployment Rate | 4.3% | 4.3% |

| 2-Year Treasury Yield | 4.01% | 3.87% |

| 10-Year Treasury Yield | 4.44% | 4.37% |

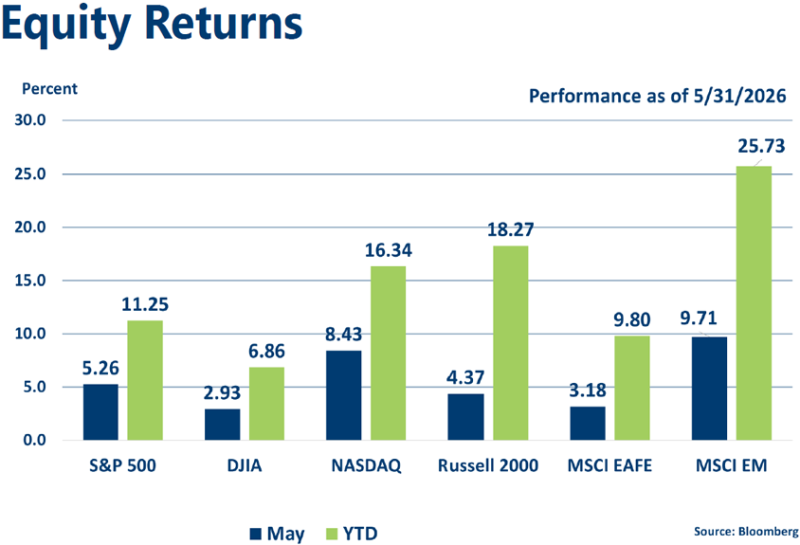

Equities

- Despite narrow leadership and a growing gap between winners and losers, equity markets remained strong in May, with major indices finishing at or near record highs.

- Gains were driven mainly by AI, technology, and semiconductor stocks — without which the broader market would have been flat or negative.

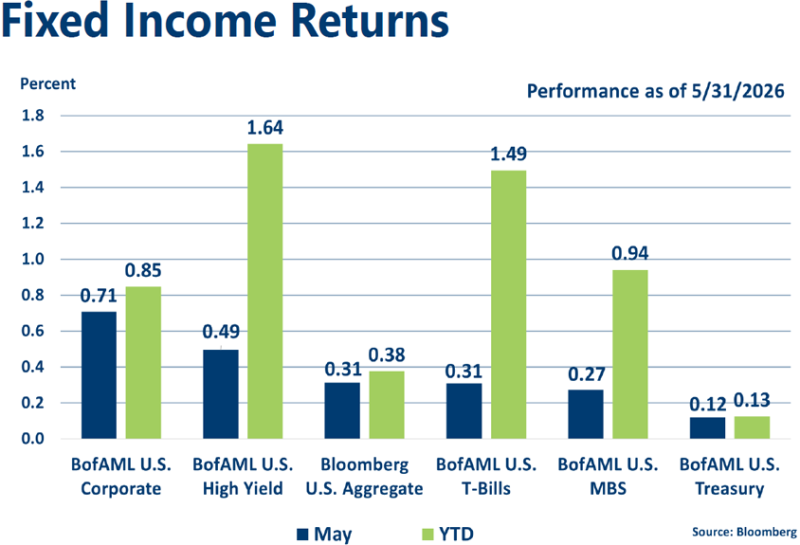

Fixed income

- Treasury yields are rising, which improves income, but it also increases the risk of price declines if inflation and fiscal pressures push rates even higher.

- The Fed’s tone has grown increasingly hawkish, with futures markets now implying about a 50% chance of a rate hike by year-end.

Strategic outlook

- Near-term caution toward equities is advisable, given heightened risks from geopolitical instability, trade uncertainty, and the potential for renewed inflationary pressures alongside an economic slowdown.

- Near-average expected returns projected for fixed income with the Fed on pause and rates reflective of economic conditions.

- Above-average volatility is likely given central bank involvement and geopolitical uncertainty.

|

Learning Center articles, guides, blogs, podcasts, and videos are for informational purposes only and are not an advertisement for a product or service. The accuracy and completeness is not guaranteed and does not constitute legal or tax advice. Please consult with your own tax, legal, and financial advisors.