Market Recap: February 2026

March 03, 2026

Market commentary

- Although the economy continued to grow, a lengthy government shutdown temporarily pulled fourth-quarter GDP down to 1.4%.

- A Supreme Court ruling eliminated many of the old tariffs, but new ones are already being implemented, leaving tariffs as a major uncertainty for the economy.

- Even with low confidence readings, consumer spending remains solid thanks in part to wealth gains from the stock market.

- Manufacturing activity stayed in expansion territory for the second straight month, according to the ISM Index.

- Geopolitical risks tied to the Iran conflict are creating volatility in oil markets, as potential disruptions in the Strait of Hormuz could feed into higher inflation.

Select economic and market data

Statistic (monthly unless noted) |

Current |

Previous |

|---|---|---|

| U.S. GDP (quarterly) | 1.4% | 4.4% |

| Consumer Confidence | 91.2 | 89.0 |

| Consumer Price Index Y/Y | 2.4% | 2.7% |

| Core PCE (x food & energy) | 3.0% | 2.8% |

| ISM Manufacturing Index | 52.4 | 52.6 |

| Unemployment Rate | 4.3% | 4.4% |

| 2-Year Treasury Yield | 3.38% | 3.52% |

| 10-Year Treasury Yield | 3.94% | 4.24% |

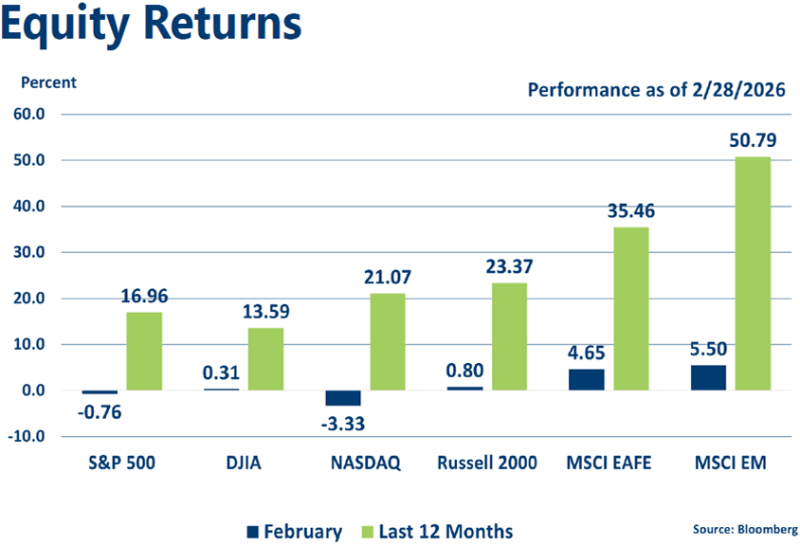

Equities

- February saw the S&P 500 and Nasdaq decline as investors rotated away from mega-cap leaders and toward value sectors including utilities, energy, materials, staples, and industrials.

- Non-U.S. markets continued to outperform, highlighted by the MSCI Emerging Markets Index’s impressive 12-month gain of over 50%.

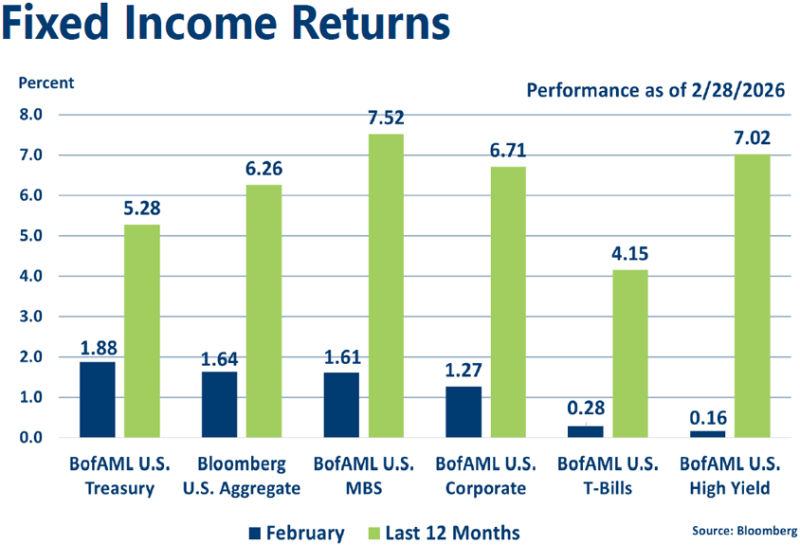

Fixed income

- The Fed remains on hold, arguing that structural shifts like AI aren’t enough to justify rate cuts without clearer signs of falling inflation.

- Treasury yields fell in February, boosting returns for investment-grade bonds, while high-yield debt lagged alongside the weaker equity market.

Strategic outlook

- Some caution warranted on equities in the near-term, particularly in large-cap stocks with above-average valuations; currently favoring small-cap and mid-cap domestic stocks longer-term.

- Near-average expected returns projected for fixed income with the Fed on pause and rates reflective of economic conditions.

- Above-average volatility is likely given central bank involvement and geopolitical uncertainty.

|

Learning Center articles, guides, blogs, podcasts, and videos are for informational purposes only and are not an advertisement for a product or service. The accuracy and completeness is not guaranteed and does not constitute legal or tax advice. Please consult with your own tax, legal, and financial advisors.